Are You in the Retirement Risk Zone?

Are you in the Retirement Risk Zone? The Retirement Risk Zone is the five to 10 years just before and after your retirement date. It’s the critical time when short-term losses can have negative long-term effects since there’s little time left for investments to recover.

As a CFP for over 20 years, I meet many individuals, families and business owners and what I find most common is that they don’t have a written financial plan. The most common goal that they want is an assessment of their current Retirement Income Plan to determine if it’s on track and if it’s not what needs to be changed. That is the focus of my company, Advantage Wealth Planning.

Common Questions

- Am I saving enough for retirement?

- When can I retire?

- How long will my money last?

- When to convert RRSPs to RRIFs and how quickly should RRIFs be drawn down?

- Should we buy an annuity to fund retirement?

- What are my Canada Pension Plan benefits? When is it best to start CPP?

- What are my Old Age Security options and when is it best to start?

- How do I setup a proper investment portfolio for my risk tolerance?

- Am I invested in the proper products?

- Will my investments last my lifetime?

- Are my investments suitable for my risk tolerance?

- How is my income taxed?

The list is virtually endless!

Financial Planning Service Offered

Advantage Wealth Planning offered two choices of Financial Planning solutions for clients until December 31, 2022. The Fee-for-Service Financial Plan is currently unavailable.

Advantage Wealth Planning proudly offers a Full-Service Financial Plan. The plan includes all six-steps from goal setting to implementation and monitoring in a written format with recommendations. Once the asset transfer is complete, the initial financial plan is completed at no additional cost. Subsequent financial plan updates, at no additional cost, are held annually or more often when major financial decisions are being considered. The minimum asset level for new clients is $150K. Investment management is by a third-party investment manager (that we have worked with for over 15 years), using pooled-funds, ETFs and individual securities. The investment manager and financial planner compensation are bundled into one transparent fee. Larger accounts are eligible to receive reduced fees and non-registered account fees may also be tax-deductible.

![]()

Latest Articles

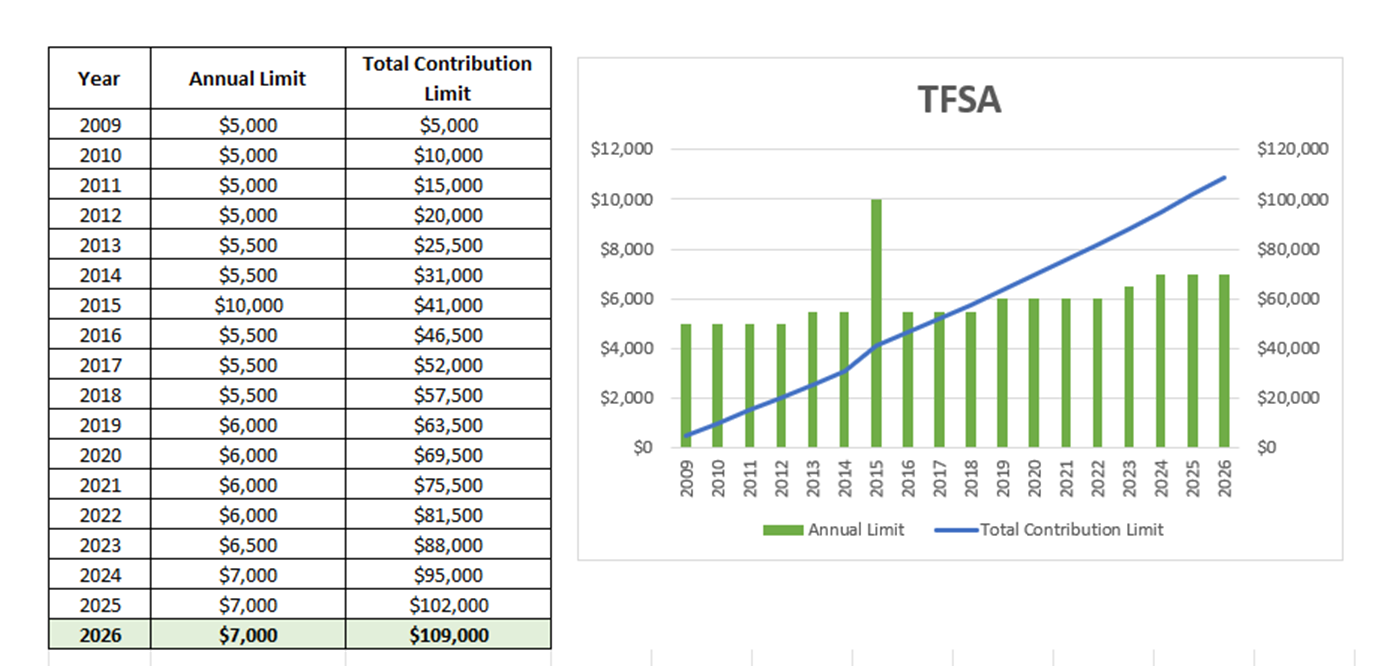

A Guide to the 2026 Tax Free Saving Account (TFSA)

Tax Free Saving Account (TFSA) Updates for 2026 Canadians can earn tax-free investment returns using the plan referred to as the Tax-Free Savings Account (TFSA). Often I am asked, “should I contribute to an RRSP or a TFSA”. The two plans are very different. You get a tax deduction for contributions to an RRSP but […]

![]()

2025 RRSP Contribution Limits and 2024 RRSP Contribution Deadline

The Registered Retirement Savings Plan (RRSP) is an investment plan used by Canadians to save for retirement. Contributions are tax deductible for tax purposes, however there is a limit. The contribution rate is 18% of earned income up to a $31,560 which equates to an earned income of $175,333.33. This amount is reduced if you […]

![]()

A Guide to the 2025 Tax Free Saving Account (TFSA)

Tax Free Saving Account (TFSA) Updates for 2026 Canadians can earn tax-free investment returns using the plan referred to as the Tax-Free Savings Account (TFSA). Often I am asked, “should I contribute to an RRSP or a TFSA”. The two plans are very different. You get a tax deduction for contributions to an RRSP but […]

![]()

Consumer Price Index, CPI

As of June 2024, the annual change in the CPI was 2.7%. This article explains what the CPI is and what it means for Canadian consumers. What is the CPI? The Consumer Price Index (CPI) represents changes in prices as experienced by Canadian consumers. It measures price change by comparing, through time, the cost of […]

![]()

April 15, 2024 Canadian Federal Budget

There are items in the recent Federal Budget that may be important to you, your family and your business. Here’s a 2024 Canadian Federal Budget handy tip sheet to help you manage your finances from Empire Life. Read here or download a copy using the link 2024 Canadian Federal Budget.

![]()